{kind=link}

Which Best Explains Why Banks Consider Interest on Loans? – Knowledge of whether the banks see interest on loans as important is essential to the appreciation of the operations of financial institutions. Loan interest is the foundation of the revenue generation of the banks because the income is utilised in their business processes to partake in lending to others and earn profit. The interest you pay when you borrow money is not a mere fee, but it acts as lifeblood and helps banks to make more financial products and services available. It is quite important to appreciate the fact that the key purpose of interest in loans is to better understand the larger role of the banking sector as well as its soundness.

Table of Contents

Why Banks Consider Interest on Loans? – Key Highlights

- Interest on money borrowed is the main revenue stream available to banks and consequently has a direct effect on profits, and hence the solvency of the bank.

- The interest income enables banks to meet the necessary operating expenses and provide customer services such as savings accounts and credit cards.

- Net interest margin between the interest charged on borrowed money and the interest paid on deposits, is important to the business model of the bank.

- Both the interest rates in the market and the demand for loans considerably influence the overall profitability of a particular bank.

- The absence of interest income could not allow banks to support lending and the provision of essential banking services.

Explain Briefly Why Banks Consider Interest on Loans?

In the case of banks, receiving interest on loans is not a mere business process, but it is an essential profit maker and lifeline of any bank. Other sources of traditional banking revenue are insignificant when compared to the interest revenue, which is the main component of loans. As a bank advances money, it requires an interest rate that guarantees it a constant flow of income, which facilitates its main activities.

Such a sustained flow of finances is important to cover operational expenses and absorb financial risks. Interest earned by banks helps them to remain afloat, provide new loans, and sustain the market in the dynamic financial services industry.

How Interest Income Contributes to Bank Profitability?

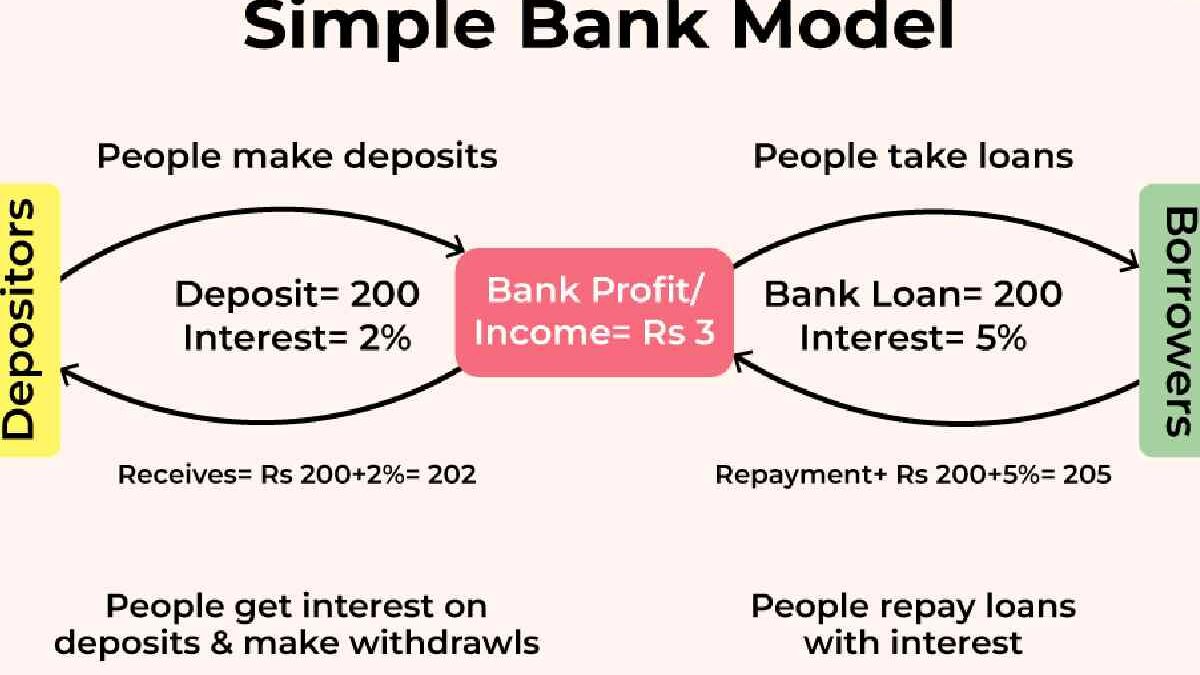

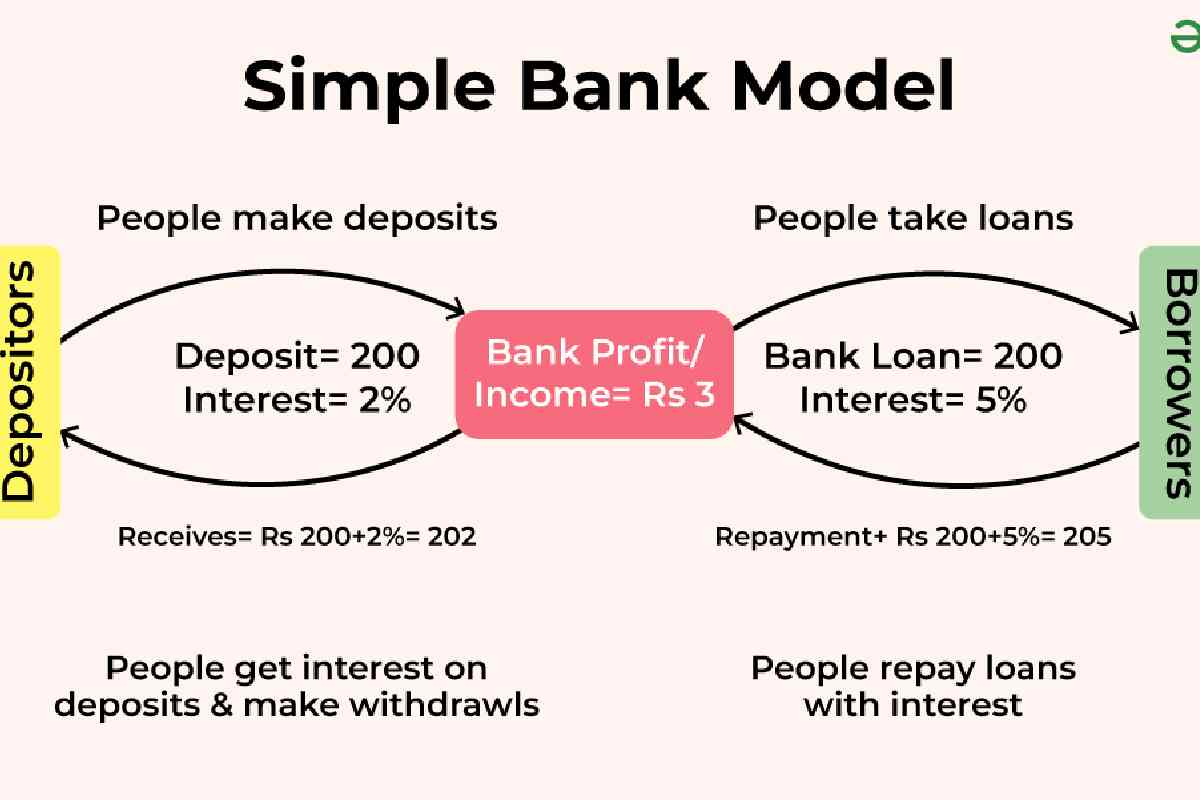

The greatest profitability of banks lies in the interest receivable by the recipients. When a bank lends money to someone /she earns a payment of interest over time. The money paid increases the interest earnings accrued to the bank, which is an essential indicator of its performance.

Businesses that need capital quickly often seek specialized instruments; for these situations, a merchant cash advance offers a flexible and rapid alternative funding solution that aligns closely with a business’s daily sales performance.

One of the major factors that helps banks measure profitability is by looking at their returns on assets, which in many cases are based on efficient lending and earning an income on loans that offer dependable income. The net interest margin is defined as the difference between the interest received by the banks when lending and the interest that is paid by the banks on the deposits. The margin is normally adopted as a standard to determine the health of a bank in terms of performance.

| Key Term

|

Meaning & Significance

|

| Interest Income

|

Money earned from loans made by the bank

|

| Net Interest Margin

|

Difference between loan interest earned and deposit interest paid, as a % of average earning assets

|

| Return on Assets (ROA)

|

An indicator of how profitable a bank is relative to its total assets |

| Lending

|

The act of giving out loans to borrowers, generating revenue through interest

|

| Financial Performance

|

Generally, profitability, efficiency, and sustainability measurement

|

The importance of interest earnings to the businesses of a bank can be expounded by the fact that without healthy interest income, the banks would find it difficult to sustain positive performance and attain shareholder expectations.

The Role of Interest in Covering Operating Costs and Supporting Services

Interest paid on loans goes beyond increasing the bottom line; it is used to offset the numerous costs of operations that banks have to incur. The payment of staff salaries, the upgrade in technology, and any element of the bank’s functioning is dependent on the continuous flow of interest money.

Through this source of revenue, the banks can provide many services to you and other consumers, including savings accounts, checking accounts, and credit cards. Banks would not have money to offer such helpful services since interest income would be nil.

- Interest income can cover the day-to-day expenses such as utilities, wages of employees, and compliance costs.

- It finances innovation, the creation of digital banking products.

- The banks utilize this income in financially contributing to community lending, mortgages, as well as funding for small businesses.

Due to its stability and predictability as compared to certain other sources of income, interest on loans is regarded as the core factor of maintaining the operations of a bank and providing it with the services its customers need. This being the case, we can observe how interest is the stimulus that affects every stratum of bankingness.

Conclusion

To sum up, it is important to explain the reason why the interest on loans is taken into account by banks so as to get the definitive sense of their working framework. Interest not only acts as a major source of income earnings, but it also considerably contributes to the general profitability of banks. It assists in the payment of operating expenses, buys the necessary services of a service provider, and provides stability against rivalry in the market.

Knowledge of the significance of interest income will enable consumers to better decide on borrowing and lifetime finance plans. In case you still have some curious questions or require help to orient yourself among your opportunities at the bank, do not be afraid to ask an experienced specialist to help you.

Frequently Asked Questions

Why do banks rely more on interest from loans than on other sources of revenue?

The income from interest is a very stable, reliable form of revenue for the banks as compared to other sources of revenue that include fees and investments. This stability becomes the mainstay of sustainable banking operations and the foundation of the bank in its profit model and long-term financial model.

What would occur when banks no longer pay interest on loans?

Without interest income on loans, banks would not have the means to finance loans, as well as operations. Such loss of interest would pose a threat to the existence of the banks and interfere with conventional models of operation and access to funds by both individuals and businesses within the economy.

How is the interest banks earn on loans different from the interest paid on deposits?

Interest on loans is earned on the money that banks charge their lending clients, whereas interest on deposits is what banks earn by giving their clients money who have a savings or checking account. The difference between the two, or the interest margin as it is called, is the profit that the banks receive due to the lending manner, and this is crucial to the success of the banks.